|

1/14/2019 0 Comments How to Make a Planner Vision Board

Did you know that the second Saturday of January is National Vision Board Day? With two weeks into the New Year, we've gotten our acts together and settled back into our “non-vacay” mode. As a crafty girl, I take my vision board very seriously! It has to be functional. It has to be accessible…and oh yeah…it has to look good! Now, without throwing any shade, let me say this. I've seen lots of vision boards and many of them look like ransom notes. I'm just keepin' it real! All the chopped up magazine words and images can easily come together to look like crime scene evidence rather than an inspiration. To remedy the epidemic of ransom note vision boards, I'm sharing a few of my own crafty tips for making a vision board that works! My first tip for vision boarding is to use you planner as the home of your board. Your planner is always within reach and you can reference your vision board whenever you want. By keeping a planner vision board, you'll constantly be reminded and inspired by the goals you set.

To make a planner vision board, you'll need a few crafty items:

CLICK HERE TO DOWNLOAD & PRINT YOUR JOURNAL CARDS

STEP ONE: Use a paper trimmer to cut your patterned paper to 9.25″x12″

STEP TWO: Use a scoring board to score the paper at 7″

STEP THREE: Fold the paper as shown

STEP FOUR Punch the edge of the paper with the Planner Punch Board and insert into your Happy Planner Now that you've created the base of your vision board, you can get to work adding all the goals and decorative elements that will make this board an inspiration all year long! Here are a few tips for how I but my vision board together!

TIP: Use journaling cards or ephemera frames on the outer fold of your vision board. This can be a place to write down all your main goals for the month, year, season…whatever!

TIP: Use the inner portion of the paper for placing images, inspirational phrases and notes. This can be the place where you dive into each of your goals and create a more traditional vision board.

TIP: Print off a few extra journaling cards to use throughout the year! Vision boards are a great way to jump start your motivation and these journaling cards are quick and easy ways to keep you going.

Happy vision boarding! Be sure to tag #DamaskLove and @DamaskLove on Instagram to show how you're creating your own vision board this year. And if you're in the mood for even more vision board inspiration, head over to Live Abode where we're sharing some awesome tips for creating your own vision board party!

0 Comments

If we were to take a guess, we would imagine that cockroaches are at the top of the list of pests that people want to avoid. For one, they aren't very appealing as far as critters go, nothing cute and cuddly about a roach. Two, they are dirty pests that spend much of their time living in filth. The good news is that there are ways to protect your Souderton home against cockroaches in 2019.

The post 7 Trends in Kitchen Cabinet Painting appeared first on Denver Paint Contractor. 1/12/2019 0 Comments Cozy in Coastal MaineMaine is famous for beautiful summers with refreshing temperatures, ocean breezes, and plenty of outdoor activities. The winter season is pretty fabulous too, and there are many offerings to entertain the adventure enthusiast or the homebody. Maine's various ski mountains attract visitors from all over New England and beyond. Frozen lakes and ponds are perfect for family ice skating or a vigorous round of hockey; and there are numerous trails for snowshoeing or cross-country skiing. Whether you wish to go out and enjoy one of these brisk winter adventures, or simply cozy up by the fire, these stunning Maine homes have got you covered. Aspinwall Bremen Long Island, Maine

Undercliff Cottage | Camden, Maine

Sears Cottage | Islesboro, Maine

Periwinkle Beach | Islesboro, Maine

Otter Creek Lane | Islesboro, Maine

Northeast Point | Camden, ME

Dark Harbor House | Islesboro, Maine

260 Bay View Street | Camden, Maine

The post Cozy in Coastal Maine appeared first on LandVest Blog. Bathroom remodeling is filled with difficult decisions, and sometimes the first ones are the hardest… like what to let go and what to keep! We shared some ideas with you recently, and now we're back with part two, via The Recorder Online, to help you decide what to keep when you remodel your bath! Tired of the tub?

We relayed the advice about what to do with your jetted tub – namely, get rid of it. But that doesn't mean just ban the bath!

The outside of a clawfoot tub can often be painted to match your other decor. And the inside, if it has seen better days, may be a candidate for reglazing. Don't get sunk at the sink!Even if your sink is functional, it can be… well… less than ideal.

It may be as simple as a new aerator, or as involved as a new basin. Either way, the sink is something you use (hopefully, anyway) every time you use the bathroom. It's deserving of an upgrade. Mirror mirror, on the wall!

In the future, archeologists may be resigned to using our bathroom mirrors to determine the relative age of our homes. And it would work. Your mirror will date your bathroom faster than anything else.

If you can't do away with the dreaded mirror wall, try adding a frame or shelves to tone it down a bit!

Can you think of other items that should definitely stay – or go! – during a bathroom remodel? Let us know your thoughts in the comments! The post Decisions, Decisions… More of What to Keep When You Remodel the Bath! appeared first on Welcome to O'Gorman Brothers Bath Fitter. 1/10/2019 0 Comments Modern Hardware For Your CabinetsOver my 2-week Winter Break I managed to cross off tons of big house projects that had been on my list for ages-including painting the dated wood dresser in our downstairs hall bathroom. I'm planning to share the project (terrifying before-and-after photos and all!) soon, but let's just say the piece needed a total overhaul, from top to bottom. Brand new modern hardware was the perfect finishing touch to complete the furniture project, and I ended up falling down the rabbit hole of pretty pulls when I started working to choose the right one for our dresser. Scroll on to see a few that we considered, and stay tuned next month to see what we ended up pulling the trigger on for our bathroom dresser. Modern Hardware For Your Cabinets1. Dish Knob 2. Mabel Knob 3. Quinn Handle 4. Mid-Century Modern Solid Brass Drawer Knob 5. Galley Pull 8. Alberta Pull 9. Empire Knob 11. 4″ Bronze Corrugated Handle With Back Plate Do you have a favorite from my list of 12? Number 11 was actually a top contender for our dresser for a while there before I decided to go in a slightly different direction. I'm surprised that I considered going with something a little more transitional, but am also excited to notice that my tastes might be evolving a bit. Have you tried updating your own cabinets or drawers with new hardware lately? It's such a budget-friendly way to completely change the look of furniture or cabinets in your home. I can't recommend this type of DIY more! *I earn a small percentage from purchases made using the affiliate links above. Affiliate links are not sponsored. Rest assured that I never recommend products we wouldn't use or don't already love ourselves. The post Modern Hardware For Your Cabinets appeared first on Dream Green DIY. 1/10/2019 0 Comments New Year, New Home?

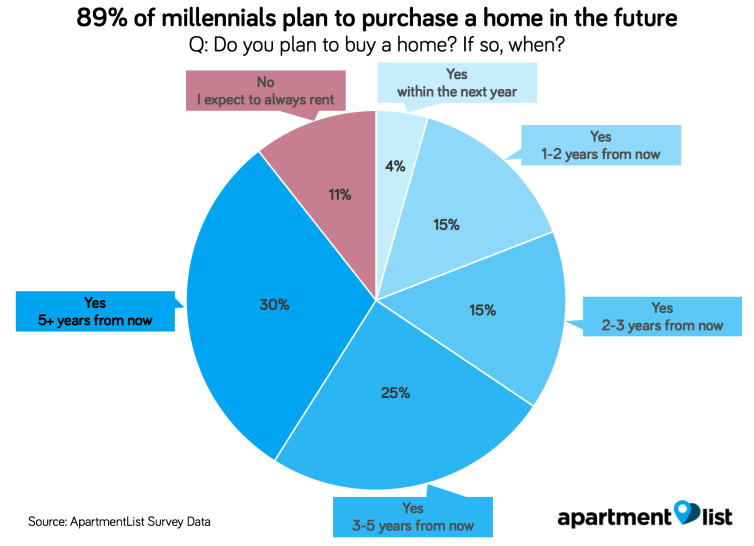

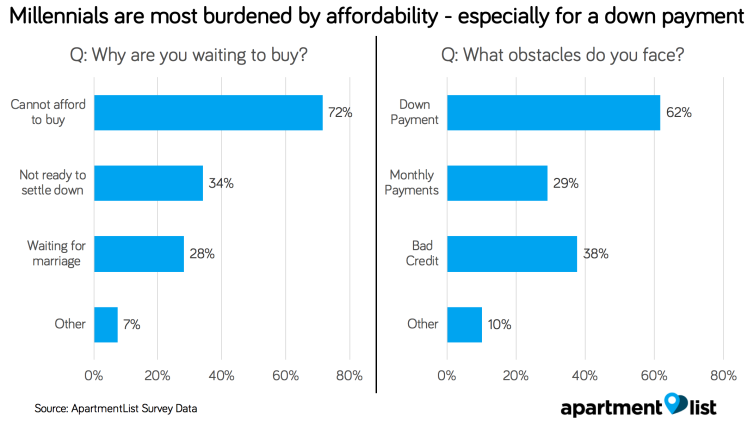

It turns out a lot of millennials want to buy a home someday - a whooping 89 percent according to a new Apartment List survey. But, just 5 percent expect to buy in 2019 and 34 percent say they will wait at least five years. Why the lag? While the dream of homeownership is strong, 72 percent cite affordability as the critical issue.

Down payment funds are primary challengeSixty-two percent of millennials specifically mention the lack of funds for a down payment. Only 11 percent have saved $10,000 or more for a home and 48 percent have zero down payment savings.

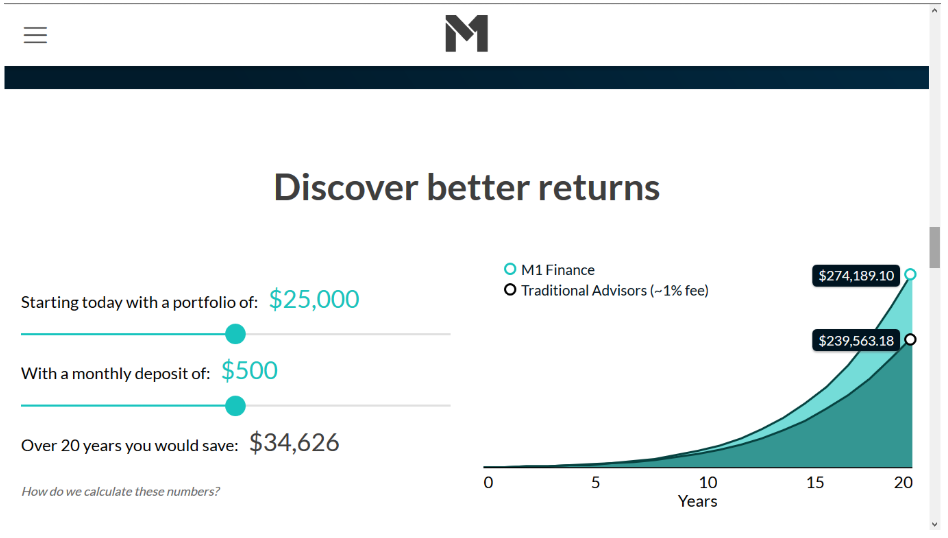

What the study overlooksThe survey also found that two-thirds of Millennial renters would require at least two decades to save enough for a 20 percent down payment on a median-priced condo in their market. What this study overlooks is that a 20 percent down payment isn't required and isn't even typical for a first-time homebuyer. The average down payment for a first-time buyer is about 7 percent today, according to the National Association of REALTORS. So, don't despair - you have options. Today, there are multiple loan programs are available with as little as 3 or 3.5 percent required as a down payment. keep reading The post New Year, New Home? appeared first on Down Payment Resource. If you've been fascinated with the idea of robo-advisors, but still prefer to go the do-it-yourself route, you need to check out M1 Finance. It's a robo-advisor for sure, but one with a unique twist: you choose your own investments. That's the self-directed part. But once you choose your investments, you get all the benefits of a robo-advisor. M1 Finance then manages your portfolio for you, including periodic rebalancing and dividend reinvesting. Your only responsibilities are to choose your investments and fund your account. It doesn't fit neatly within the description of a robo-advisor, but it's really a hybrid between robo-advisors and self-directed investing. It wouldn't be an exaggeration to say it represents the best elements of both.Interested? How M1 Finance WorksM1 Finance is based in Dallas, Texas, and was launched in 2015. The service is built around what it refers to as “Pies”. These are individual portfolios that are comprised of a mix of exchange-traded funds (ETFs) and individual stocks. ETFs are a staple of the robo-advisor universe. But individual stocks are offered by only a few providers, and when they are, they're usually selected by the robo-advisor. The use of individual stocks–and your own ability to choose which stocks and ETFs go into your pies–is what sets M1 Finance apart. It gives you complete control over the investments you'll hold. Another departure from typical robo-advisor practice is that M1 Finance does not have you complete a questionnaire to determine your risk tolerance. In this way, the platform is better for experienced investors, who are able to determine their own investment comfort level. But still, another distinguishing factor is that you can create an unlimited number of pies. You can choose existing pie templates provided by M1 Finance, or create your own. For example, you can create a technology-based pie, a socially responsible investment pie, and an emerging market pie–all at the same time. And there's no limit on the number of pies. M1 Finance then manages your portfolio using modern portfolio theory (MPT), just as other robo-advisors do. In this way, M1 Finance is both an active and passive investment platform. It's active in the sense that you select your own investments, and can change them at any time. But it's passive in the way the pies are managed. M1 Finance Investment MethodologyM1 Finance's investment methodology is really a discussion of the pie concept. Each pie can be made up of up to 100 individual “slices”, which are represented by ETFs and individual stocks. M1 Finance provides more than 60 pre-selected pies that you can choose from, or you can construct your own. There is a limitation however in that you cannot include mutual funds in your pies. In addition, individual stocks must be selected either from the New York Stock Exchange, the NASDAQ, or the BATS system. Which means you won't be able to invest in stocks that trade only on foreign exchanges. Each pie will contain general asset allocations, which you can choose to fill with investments of your choice. M1 Finance will rebalance your pies consistent with that allocation. The allocations will also be maintained as you add additional funds to each pie. You can create pies that are made up entirely of ETFs or of stocks or a combination of both. For example, you can choose a pie for FAANG stocks, that holds only positions in each of those five companies. But you can also adjust the mix. You can choose higher allocations for one or two stocks, and lower ones for the others. This flexibility gives you complete control over how you will invest your money, but within the scope of a robo-advisor platform. M1 Finance Tax AdvantagesThis area is a mixed bag. M1 Finance does offer a tax loss strategy, in which an algorithm determines which securities are sold when you withdraw funds from your account. They do this by setting a selling priority that looks like this:

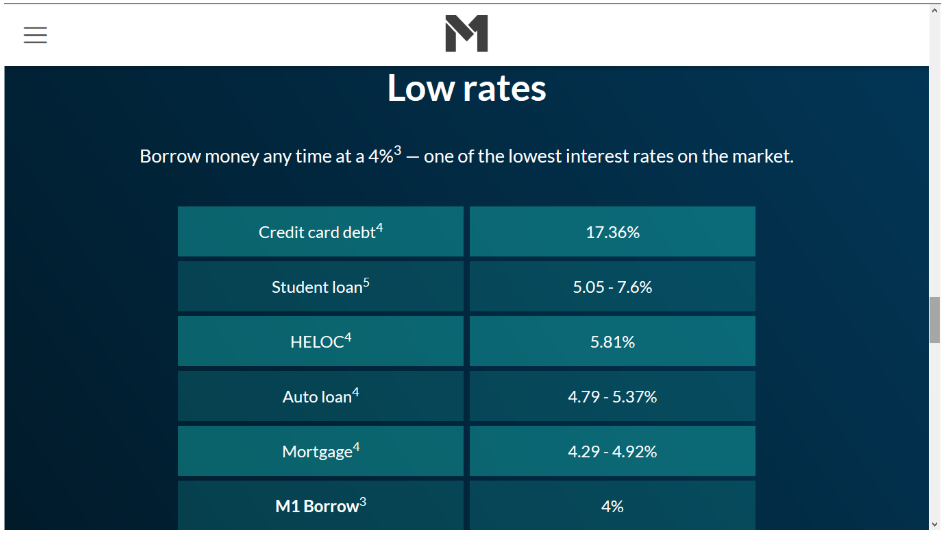

However, M1 Finance doesn't offer tax-loss harvesting, which is becoming an increasingly common feature of robo-advisors. M1 Finance Features & BenefitsAvailable accounts. M1 Finance accommodates individual and joint taxable accounts, trusts, and traditional, Roth, SEP and rollover IRA accounts. Minimum investment requirement. You can open an account with no money whatsoever. But you'll need a minimum of $100 to begin investing in a taxable account, and at least $500 in a retirement account. Account custodian. Funds invested with M1 Finance are held with Apex Clearing Corporation. M1 Finance just manages your account. As a result, your account is protected by SIPC for up to $500,000 in cash and securities, including up to $250,000 in cash. This is of course protection against broker failure, and not against losses due to market factors. M1 Finance Mobile App. The app is available for both Android (5.0 and up) and iOS (10.0 or later) devices and can be downloaded at The App Store or Google Play. Exporting tax information. Your annual investment results can be exported directly to either TurboTax or H&R Block tax preparation software. Dividend reinvestment. M1 Finance automatically reinvests your dividends once they reach $10. M1 Borrow. You can borrow up to 35% of the value of your portfolio for any purpose, and without a credit check. Once borrowed, the money can be paid back on your own terms. The interest rate is 4.00% APR as of December 7, 2018.

Since the funds borrowed represent margin against your account, you may be subject to a maintenance call if your portfolio value falls below a certain threshold. A maintenance call normally happens when your account equity falls below 30%. However additional restrictions may be placed if your portfolio is deemed to be particularly high risk. Referral program. If you refer a friend who signs up for an M1 Finance account, both you and your friend will receive $10 to invest in your respective accounts. You'll be given a unique link on the mobile app that you can share with friends by email, text, or even social media. M1 Finance customer service. You can reach M1 Finance by either phone or email, Monday through Friday, 9 am to 5 pm, Central Time. Get started with M1 Finance today. M1 Finance PricingThis is one of the most compelling features about M1 Finance. There are no fees! That means:

So how does M1 Finance make money if they don't charge fees to investors? After all, if they don't make any money, they won't be in business very long. M1 Finance explains it this way: ”Brokerages make more money via lending securities they hold, interest on cash held in a brokerage account, extending credit through margin to customers, and getting paid for distributing certain funds or to transact on various exchanges. These revenue streams are more than enough to support a strong, vibrant company. This is also true at M1 Finance, and we will make more money from transactions and holding the assets than we would from our fee.” So there you have it: a brokerage platform that admits to making its money on the back end, in favor of offering investment services to customers for free. You've gotta love the honesty, along with the fee-free service. How to Sign up with M1 FinanceTo open an account with M1 Finance, you'll need to:

You'll begin by entering your email address and creating a unique password. You'll also need to provide your name, address, and phone number.

Once you open your account, you can dive right into creating your investment pies. As discussed earlier, you can either choose from one of more than 60 pre-selected templates or make your own custom pie. The next step is to link your bank account to your M1 Finance account. From there, you can fund your account. But the link means you can also withdraw funds, as well as contribute additional money going forward. M1 Finance can automatically link to a large number of banks, saving you time inputting information. But if your bank isn't one of the choices, you can add it. Just add the name of your bank, the type of account, your bank routing number, and personal account number, and you'll be ready to go. Get started with M1 Finance today. M1 Finance Pros & ConsPros:

Cons:

Why You Should Invest with M1 FinanceM1 Finance isn't for all investors. If you're completely inexperienced, the self-directed aspect of the service may leave you taking on more than you want. There are plenty of other robo-advisors that are very well suited to completely passive investing for beginners, including Betterment and Wealthfront. But if you're an experienced investor, who prefers to go the do-it-yourself route, but doesn't want the hassles of day-to-day portfolio management, M1 Finance is the perfect robo-advisor for you. You can build your own portfolios and as many as you want. You can even select the stocks and ETFs included in your pies. But you won't have to concern yourself with rebalancing for reinvesting dividends. And you've gotta love that you can invest completely free. Unlike most robo-advisors, there's no annual advisory fee. And unlike discount brokers, there are no trading fees. Plus, you can borrow up to 35% of the value of your account at below market rates, and pay it back at your leisure. That's a powerful combination that's unmatched anywhere else in the investment universe. If you'd like more information, or you'd like to start investing, check out the M1 Finance website. The post M1 Finance Review: The Free Robo Advisor YOU Control appeared first on Part-Time Money.

One of the rules of frugal grocery shopping is to buy in bulk. Indeed, we're told to buy larger amounts of the things we like when they are on sale so that we save money in the long run. However, in some cases it's actually better to forgo buying in bulk. Here are 8 things where this is particular true:

|

1. Nuts

1. Nuts

RSS Feed

RSS Feed